NVIDIA’s decision to fold its DGX Cloud division back into engineering isn’t just a corporate restructuring, it’s a signal that the AI chip wars have entered a new phase. A new era, where even the dominant player must choose between competing with customers and securing the supply chain that fuels its empire.

In December 2025, NVIDIA executed one of the most significant strategic reversals in its recent history. The company disbanded its standalone cloud business unit, moved several hundred employees under Senior Vice President Dwight Diercks’ engineering organization.

They also effectively ended its two-year experiment to become a direct competitor to Amazon Web Services, Microsoft Azure, and Google Cloud. This Nvidia cloud computing reorganization represents far more than a simple departmental shuffle.

It reveals the structural constraints facing a hardware company that momentarily believed it could own the entire stack, from silicon to services, and the cold reality of a market where your biggest customers are also your most dangerous potential rivals.

The Nvidia cloud computing reorganization also sends a clear message to the broader technology market.

When a company with a $4.97 trillion market cap and an 86% share of the AI accelerator market decides it cannot compete in cloud services, the implications ripple across every layer of the infrastructure stack.

This article examines why NVIDIA made this pivot, what structural failures drove the decision, and how the company’s revised AI chip strategy** will reshape its relationships with hyperscalers, enterprise customers, and the emerging ecosystem of GPU cloud providers.

The Original Vision: Why NVIDIA Tried to Build a Cloud Empire

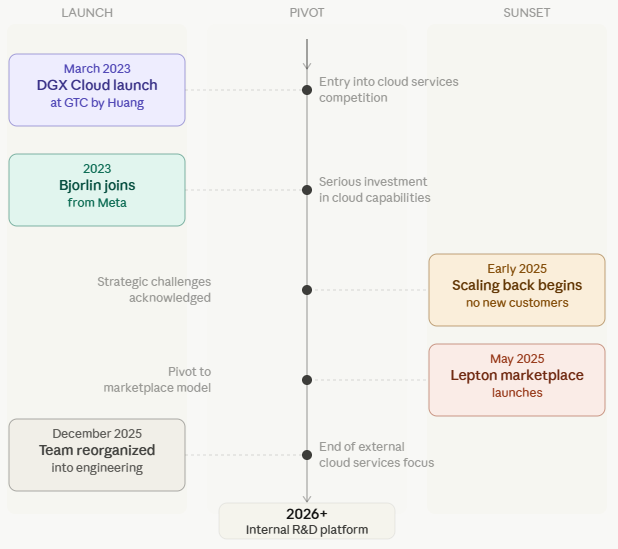

At GTC 2023, Jensen Huang stood before thousands of developers and announced DGX Cloud with the confidence of a conqueror. The pitch was straightforward: AI developers were renting NVIDIA GPUs through hyperscalers, but those cloud providers weren’t optimizing for NVIDIA’s architecture.

By building its own cloud, NVIDIA could offer better performance, deeper software integration, and crucially, a direct relationship with the developers who would determine the next decade’s computing standards.

The business case looked compelling on paper. NVIDIA had told investors that cloud services could eventually generate $150 billion in annual revenue, a figure that would exceed AWS’s current run rate.

The company hired Alexis Black Bjorlin from Meta in 2023, gave her a direct reporting line to Huang, and staffed the division with hundreds of engineers and sales professionals. Early customers including ServiceNow, SAP, and Amdocs were announced with fanfare.

But the vision collided with three structural realities that no amount of optimism could overcome. The Nvidia cloud computing reorganization that followed in late 2025 was the inevitable result of these structural misalignments.

The Three Structural Failures That Killed DGX Cloud as a Product

1. The Architecture Problem: You Can’t Support What You Don’t Control

DGX Cloud’s fatal flaw was architectural. The service didn’t run on NVIDIA-owned data centers, it ran inside third-party facilities operated by AWS, Google, and Microsoft.

When a customer encountered a performance issue, NVIDIA’s engineers couldn’t simply walk into the server room and diagnose the problem. They needed permission, coordination, and cross-company troubleshooting protocols that added hours or days to resolution times.

Former team members described this as a support nightmare. A fix implemented in one cloud provider’s data center often couldn’t be replicated in others because the underlying infrastructure, networking configurations, and virtualization layers differed.

NVIDIA was selling a premium performance promise while operating on infrastructure it didn’t fully control, a contradiction that enterprise customers quickly recognized.

The company attempted to solve this with DGX Cloud Lepton, a marketplace launched in May 2025 that allowed cloud providers to list unused GPU capacity. Providers including CoreWeave, Lambda, Crusoe, and Foxconn signed on.

But the marketplace model introduced its own complexity: customers now had to navigate multiple support channels depending on which provider hosted their workload, and NVIDIA remained the middleman responsible for a unified experience it couldn’t actually deliver.

2. The Customer Conflict: Competing With Your Biggest Buyers

Here’s where the strategy became genuinely untenable. AWS, Google, and Microsoft aren’t just NVIDIA’s competitors in cloud services, they’re its largest chip customers.

In 2025, these four hyperscalers collectively spent approximately $650 billion on AI infrastructure, with NVIDIA capturing roughly 86% of the AI accelerator market by revenue.

When NVIDIA tried to sell cloud services directly to enterprises, it was effectively telling its biggest customers: “We’ll take the end-user relationship you spent decades building, and we’ll use your own data centers to do it.”

Jensen Huang understood this tension intuitively. According to multiple sources familiar with internal discussions, Huang was reluctant to expand DGX Cloud aggressively because he recognized that alienating hyperscalers would threaten the chip orders that currently generate the majority of NVIDIA’s $253 billion annual revenue.

The cloud business was projected to reach $150 billion someday, but the chip business was already delivering $39.1 billion per quarter in Data Center revenue alone. The math was brutal: risk a certain $150 billion+ annual chip business for a speculative $150 billion cloud future.

This dynamic isn’t unique to NVIDIA. It’s the fundamental tension that every component supplier faces when considering vertical integration. Intel tried to build a cloud business with McAfee and failed.

Qualcomm’s attempts to enter server markets have been similarly constrained. The difference is that NVIDIA’s dominance in AI chips made the conflict more acute, its cloud ambitions threatened the very partners whose demand had created its monopoly.

3. The Ecosystem Paradox: Funding Competitors to Your Own Cloud

Perhaps the most bizarre aspect of NVIDIA’s cloud strategy was its simultaneous investment in companies that directly competed with DGX Cloud.

NVIDIA provided funding and strategic support to emerging cloud providers like CoreWeave and Lambda, which built GPU-focused clouds specifically designed to attract customers who might otherwise use DGX Cloud.

These “NVIDIA Cloud Partners” (NCPs) received preferential chip allocation, technical support, and co-marketing, while NVIDIA’s internal cloud team tried to win the same customers.

This wasn’t corporate confusion. It was strategic hedging. NVIDIA recognized that it couldn’t build a global cloud footprint to rival AWS, so it tried to cultivate an ecosystem of smaller providers that would collectively offer an alternative.

But this ecosystem approach undermined the economics of DGX Cloud. Why would a customer choose NVIDIA’s branded service when CoreWeave offered similar hardware with more flexible terms and lower prices?

The result was predictable: DGX Cloud struggled to attract sufficient customers to justify its operational costs, while the NCPs thrived. By late 2025, NVIDIA had effectively created a competitive market for GPU cloud services that included everyone except itself. The Nvidia cloud computing reorganization became the only logical path forward.

What the NVIDIA Cloud Computing Reorganization Actually Looks Like

The December 2025 restructuring moved several hundred DGX Cloud employees into NVIDIA’s Engineering and Operations organization under Dwight Diercks, who oversees software engineering and reports directly to Huang. Alexis Black Bjorlin, the executive hired from Meta to lead the cloud division, is seeking a new role within the company. Several other senior leaders have departed entirely.

The restructured team’s mission has shifted fundamentally. Instead of selling cloud services to external enterprises, DGX Cloud now serves as NVIDIA’s internal AI proving ground.

Engineers use the infrastructure to develop open-source foundation models, including the Nemotron family, validate new system architectures, and run production AI workloads for robotics and autonomous driving research.

The software, operational patterns, and infrastructure insights developed internally are then externalized through NVIDIA DSX OS, an open-source operating layer designed to help cloud partners build their own AI factories.

This is a genuinely clever pivot. Rather than competing with cloud providers, NVIDIA is using its internal infrastructure to make those providers better at running NVIDIA hardware. The company becomes the architect of the ecosystem rather than a participant in it.

This revised approach to Nvidia cloud computing reorganization demonstrates how a market leader can retreat from one battlefield while strengthening its position on another.

The Financial Reality: Why $150 Billion Became a Write-Off

NVIDIA’s $150 billion cloud revenue projection wasn’t merely optimistic, it was structurally impossible given the company’s other commitments. The company has stated it plans to spend $26 billion over the coming years renting servers from cloud providers for its own AI research. This makes NVIDIA one of the largest renters of its own chips, a peculiar position that highlights where its priorities actually lie.

Consider economics. NVIDIA’s Data Center segment generated $39.1 billion in Q1 fiscal 2026 alone, with full-year fiscal 2025 revenue exceeding $115 billion. The company holds approximately $53 billion in cash and carries minimal debt.

It doesn’t need cloud revenue to survive, it needs cloud partnerships to maintain chip demand. The $150 billion projection was always a narrative device for investor presentations, not a realistic business plan.

Abandoning it costs NVIDIA nothing in practical terms while preserving relationships worth hundreds of billions in future chip orders.

The Competitive Landscape: Hyperscaler Competition and Custom Silicon

Hyperscalers Are Building Their Own Chips

The threat that originally motivated DGX Cloud hasn’t disappeared, it’s intensified. Google continues developing TPU v6 Trillium with 67% better energy efficiency than its predecessor. AWS has aggressively cut Trainium 2 prices and is reportedly in discussions with OpenAI about adoption. Meta is considering spending tens of billions on Google TPUs. Microsoft’s Maia 200 is entering production.

These custom silicon efforts won’t displace NVIDIA immediately. The company still holds approximately 86% of the AI accelerator market by revenue, and its CUDA ecosystem creates switching costs measured in years, not quarters.

But the trend is clear: hyperscalers are investing billions to reduce their dependency on a single supplier. NVIDIA’s cloud retreat removes one irritant from these relationships, buying goodwill that may slow the transition to alternative chips.

The hyperscaler competition in custom silicon represents the most significant long-term threat to NVIDIA’s business model. While the company maintains dominant market share today, the combination of Google’s TPU, AWS Trainium, Microsoft Maia, and Meta MTIA creates a fragmented landscape where NVIDIA must compete not just on performance but on ecosystem stickiness.

The Nvidia cloud computing reorganization is, in part, a response to this hyperscaler competition by removing itself as a direct competitor, NVIDIA hopes to slow the pace at which its customers develop alternatives.

AMD and Broadcom Are Catching Up

AMD’s Q1 2026 Data Center revenue reached $5.8 billion, up 57% year-over-year, with the MI355X gaining traction among hyperscalers seeking a second source. Broadcom reported $8.4 billion in AI semiconductor revenue in Q1 fiscal 2026, a 106% increase, with custom XPU customers expanding from five to six hyperscalers including OpenAI. The competitive pressure is real, even if NVIDIA’s absolute dominance remains unchallenged.

NVIDIA’s best defense isn’t a cloud business, it’s ensuring that its chips remain indispensable. That requires relentless R&D focus, not distracted competition with customers. The reorganization frees engineering resources to concentrate on what the company does better than anyone else: designing the most powerful AI accelerators on the planet.

What This Means for Enterprise Customers and Developers

For enterprises evaluating AI infrastructure, the reorganization clarifies the market structure. NVIDIA will remain a chip and software platform company, not a cloud services provider. If you want managed GPU infrastructure, you’ll buy it from AWS, Google, Microsoft, or specialized providers like CoreWeave and Lambda, not from NVIDIA directly.

This is arguably better for customers. The hyperscalers have decades of experience building reliable, scalable cloud services. NVIDIA’s expertise lies in silicon and software optimization. By focusing on its strengths, NVIDIA ensures that the chips running in third-party clouds perform better than they would in a vertically integrated but operationally immature NVIDIA-owned service.

For developers, the shift means continued access to NVIDIA’s software stack—CUDA, TensorRT, Triton, through whatever cloud provider they prefer. The DSX OS initiative promises to standardize performance across providers, reducing the lock-in risk of choosing any single platform.

Expert Analysis: Is This a Retreat or a Realignment?

Having covered the semiconductor industry for over a decade, I’ve watched multiple hardware companies attempt vertical integration into services. Intel’s McAfee acquisition, Cisco’s attempts at cloud software, and Qualcomm’s server ambitions all followed similar patterns: initial excitement, strategic confusion, and eventual retreat. NVIDIA’s cloud experiment lasted only two years, remarkably short, suggesting the company recognized the mismatch quickly rather than doubling down on a failing strategy.

But calling this a “retreat” misses the nuance. NVIDIA isn’t leaving the cloud business; it’s redefining its role within it. The company will continue spending $26 billion renting cloud capacity, continue developing AI models on that infrastructure, and continue selling the resulting software and reference architectures to cloud partners. It’s a platform strategy, not a product strategy, and platforms often generate more sustainable value than direct competition.

The real question is whether this Nvidia cloud computing reorganization comes too late. By spending two years building a cloud sales organization, NVIDIA may have distracted engineering talent from the core chip development that determines its long-term competitiveness. The Blackwell Ultra and Vera Rubin architectures announced at GTC 2025 are impressive, but AMD’s MI355X and Broadcom’s custom silicon are closing the gap. In a market where HBM memory supply remains constrained through 2028, every quarter of focused R&D matters.

My assessment: this was the right decision made at the right time. NVIDIA’s $4.97 trillion market cap rests on its position as the indispensable AI infrastructure provider. Competing with customers threatened that position. The Nvidia cloud computing reorganization preserves the relationships that matter while redirecting resources toward the innovation that sustains them.

Key Timeline: NVIDIA’s Cloud Strategy Evolution

Conclusion: The Pragmatism of Power

The Nvidia cloud computing reorganization teaches a lesson that Silicon Valley often forgets: dominance in one layer of the technology stack doesn’t guarantee success in adjacent layers.

NVIDIA’s 86% market share in AI accelerators gave it the confidence to challenge the cloud establishment, but that same dominance made the challenge strategically untenable. When your customers are also your competitors, vertical integration becomes a high-stakes balancing act that rarely ends well.

Jensen Huang’s decision to fold the cloud team back into engineering reflects the pragmatism that has defined his tenure. He recognized that NVIDIA’s $4.97 trillion valuation rests on chip supremacy, not service revenue, and acted before the cloud experiment could damage the relationships that matter.

The Nvidia cloud computing reorganization isn’t an admission of failure, it’s an affirmation of focus. In the AI infrastructure wars of the next decade, the companies that win will be those that know exactly what they are and what they aren’t. NVIDIA has just made that distinction unmistakably clear.